Nonprofits with compensated workers must respect applicable laws governing the distinction between employees and independent contractor. Getting it wrong can result in significant risk exposure to the organizations and even personal liability to board members.

For example, nonprofits that misclassify workers as independent contractors may be responsible for unpaid payroll taxes, interest, and penalties (and board members have in some cases been held personally liable for such amounts), and also may be liable to their workers for noncompliance with employment laws and failure to provide such workers with the requisite employee benefits.

Unfortunately, the distinction between employees and independent contractors isn’t very clear. And there are different, often inconsistent, laws that apply for different jurisdictions and purposes. For example, the IRS’s common law-based guidance is very different from California’s AB 2257 (which modified its better known predecessor AB 5), which is much more likely to result in employee classification.

As a result, many nonprofits are failing to properly classify their workers. And one area in which this problem arises is with the classification of compensated officers, including anyone holding the responsibilities of the CEO regardless of their title (which commonly is Executive Director).

California Law

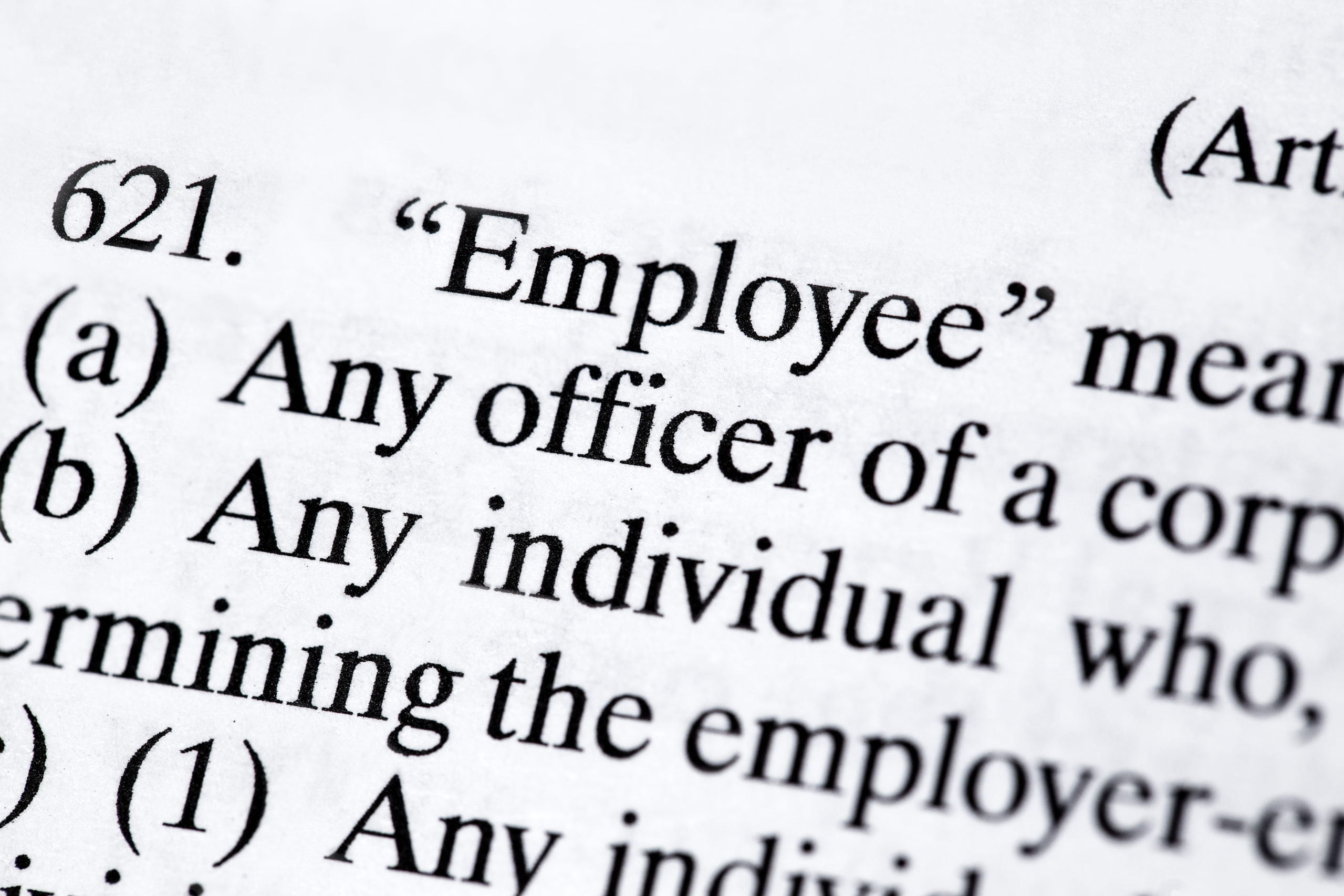

Under California law, we have the following provision as guidance:

“Employee” means all of the following:

(a) Any officer of a corporation.

CA UIC Sec. 621

The California Employment Development Department also cites this provision in its Information Sheet: Statutory Employees.

A statutory employee is defined as an employee by law under a specific statute. Generally, most individuals are determined to be employees under common law (see Information Sheet: Employment, DE 231). However, certain groups of workers have been specifically covered by the law for UI, ETT, and SDI purposes. These groups are considered statutory employees.

Corporate Officers as Statutory Employees

Under Section 621(a) of the California Unemployment Insurance Code (CUIC), a statutory employee includes any officer of a corporation.

Refer to Information Sheet: Payments to Corporate Officers, DE 231PC, for additional information.

So, for most purposes, the classification issue for nonprofit officers serving in California seems clear. They are employees by operation of statutory law. Further, even if Section 621(a) did not apply, it would be difficult to argue that a corporate officer is an independent contractor under the ABC Test now codified by Section 2775(b)(a) of the California Labor Code, which provides in pertinent part:

For purposes of this code and the Unemployment Insurance Code, and for the purposes of wage orders of the Industrial Welfare Commission, a person providing labor or services for remuneration shall be considered an employee rather than an independent contractor unless the hiring entity demonstrates that all of the following conditions are satisfied:

(A) The person is free from the control and direction of the hiring entity in connection with the performance of the work, both under the contract for the performance of the work and in fact.

(B) The person performs work that is outside the usual course of the hiring entity’s business.

(C) The person is customarily engaged in an independently established trade, occupation, or business of the same nature as that involved in the work performed.

(emphasis added)

Federal Law

Updated thanks to Patrick Anderson of Public Counsel

Under Section 3121(d) of the Internal Revenue Code, an employee includes “any officer of a corporation”, but the accompanying Treasury Regulations provides more nuance:

Generally, an officer of a corporation is an employee of the corporation. However, an officer of a corporation who as such does not perform any services or performs only minor services and who neither receives nor is entitled to receive, directly or indirectly, any remuneration is considered not to be an employee of the corporation.

26 CFR § 31.3121(d)-1

The regulation cited above seems flawed as someone who neither receives nor is entitled to receive any remuneration is certainly not an employee, which may leave open the question of whether a compensated officer of a corporation who performs no services or only minor services is always an employee by operation of law. For customary officer positions like president, treasurer, and secretary, it would be a safe presumption that they are always employees if compensated. For officer positions simply identified as such in a corporation’s bylaws, that may not be the case. For example, an assistant social activity officer who does nothing but organize the board’s annual dinner for $100 might not automatically be categorized as an employee (this may be true under California law too). How a regulator or court might get around the black letter of the law is to question whether the purported “officer” is really an officer as intended by the statute. If not …

For federal tax law purposes, the IRS applies the common law rules, as described below:

Facts that provide evidence of the degree of control and independence fall into three categories:

- Behavioral: Does the company control or have the right to control what the worker does and how the worker does his or her job?

- Financial: Are the business aspects of the worker’s job controlled by the payer? (these include things like how worker is paid, whether expenses are reimbursed, who provides tools/supplies, etc.)

- Type of Relationship: Are there written contracts or employee type benefits (i.e. pension plan, insurance, vacation pay, etc.)? Will the relationship continue and is the work performed a key aspect of the business?

Businesses must weigh all these factors when determining whether a worker is an employee or independent contractor. Some factors may indicate that the worker is an employee, while other factors indicate that the worker is an independent contractor. There is no “magic” or set number of factors that “makes” the worker an employee or an independent contractor and no one factor stands alone in making this determination. Also, factors which are relevant in one situation may not be relevant in another.

The keys are to look at the entire relationship and consider the extent of the right to direct and control the worker. Finally, document each of the factors used in coming up with the determination.

For application of the Fair Labor Standards Act, the “economic reality” test applies.

The U.S. Supreme Court has on a number of occasions indicated that there is no single rule or test for determining whether an individual is an independent contractor or an employee for purposes of the FLSA. The Court has held that it is the total activity or situation which controls. Among the factors which the Court has considered significant are:

1. The extent to which the services rendered are an integral part of the principal’s business.

2. The permanency of the relationship.

3. The amount of the alleged contractor’s investment in facilities and equipment.

4. The nature and degree of control by the principal.

5. The alleged contractor’s opportunities for profit and loss.

6. The amount of initiative, judgment, or foresight in open market competition with others required for the success of the claimed independent contractor.

7. The degree of independent business organization and operation.

There are certain factors which are immaterial in determining whether there is an employment relationship. Such facts as the place where work is performed, the absence of a formal employment agreement, or whether an alleged independent contractor is licensed by State/local government are not considered to have a bearing on determinations as to whether there is an employment relationship. Additionally, the Supreme Court has held that the time or mode of pay does not control the determination of employee status.

Fact Sheet 13: Employment Relationship Under the Fair Labor Standards Act (FLSA)

Insurance

One clear benefit of properly classifying an officer as an employee is that they may be covered under the nonprofit’s Directors and Officers (D&O) insurance and their actions or omissions causing harm may be covered by the nonprofit’s other insurance policies. Conversely, an insurance company may deny coverage to an independent contractor and harms caused by an independent contractor.

Exception

An important “exception” to the rules above, from the perspective of the nonprofit, is where the compensated officer is an employee of another employer that is leasing the employee to the nonprofit or serving as professional employer organization (PEO) to the nonprofit. While these relationships go beyond the scope of this post, see the following resources for more information:

Compensated Directors

When nonprofits compensate their board members for their service as board members, under federal law, they generally should be classified as independent contractors because board members collectively control the nonprofit, not the other way around. Before California’s adoption of the ABC Test originally codified in AB 5, this seemed to be the observed practice in California too. However, the ABC Test (now codified in AB 2257) does create some issues (probably unintentionally), as is discussed in this article from Allen Matkins: Has California Made Directors Employees?